Fuel vs. Food: Why U.S. Edible Tallow Imports Are Rising Rapidly in 2025/26

- Demetrica

- May 20

- 3 min read

The U.S. tallow market is undergoing another notable shift, and this time the story is not only about the sheer scale of imports, but also about the changing composition of those imports. Over the last several years, the United States has rapidly transformed from a relatively modest participant in global tallow trade into the world’s largest import destination. That change has been driven overwhelmingly by booming demand for inedible tallow as a feedstock for renewable diesel and sustainable aviation fuel (SAF) production. The expansion of low-carbon fuel capacity has fundamentally reshaped global trade flows, pulling increasing volumes of rendered fats into the United States from suppliers across South America, Oceania, and Europe.

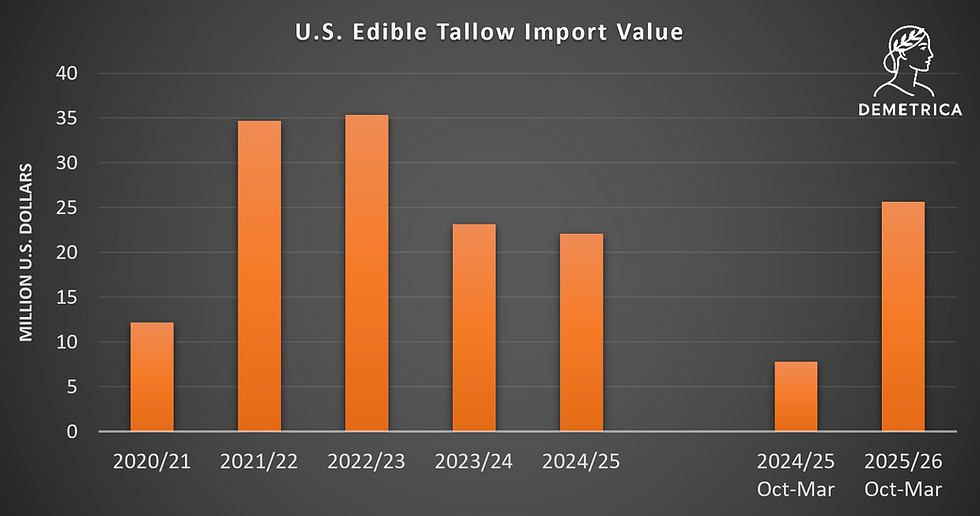

Yet while industrial demand continues to dominate the broader market narrative, early 2025/26 trade data reveal another emerging trend quietly developing in the background: a sharp rise in edible tallow imports. According to U.S. Census trade data, U.S. edible tallow imports during the October–March period of the 2025/26 marketing year increased by approximately 339% year-over-year, rising from less than 4,000 metric tons to more than 17,000 metric tons. Although the edible segment remains relatively small compared with the inedible tallow trade, the pace of growth is striking.

The value side of the market is even more revealing. In only the first half of the marketing year, the value of U.S. edible tallow imports already exceeded the total annual import value recorded during either of the previous two full marketing years. That suggests the current increase is not simply statistical noise or short-term volatility, but rather a sign of a broader structural adjustment occurring within the rendered fats complex.

Part of the explanation may lie in the renewed interest in food-grade animal fats across North America. Edible tallow has experienced a modest resurgence in recent years, supported by growing demand from specialty food manufacturers, traditional cooking applications, premium fry uses, and consumers increasingly interested in “traditional fats” and less-processed food ingredients. In some segments of the food industry, tallow has regained attention as an alternative to heavily refined vegetable oils.

At the same time, however, the broader rendered fats market has become increasingly constrained by industrial demand. Renewable diesel and SAF producers continue to aggressively absorb inedible tallow supplies, tightening availability across the entire animal fats complex. As more domestic rendered fats are diverted toward industrial production, the market increasingly requires imports across multiple grades, including edible material.

This dynamic mirrors broader developments occurring throughout the U.S. fats and oils sector. Over the last several years, domestic soybean oil and canola oil consumption for biofuel production has expanded rapidly, while food manufacturers have increasingly relied on imported alternatives such as palm oil to compensate for tightening domestic food-use supplies. In many ways, the same “fuel versus food” dynamic now appears to be emerging within the animal fats market. More domestically produced tallow is effectively being burned in fuel tanks or used in other industrial applications, leaving less available for food processing and traditional edible applications.

Another notable feature of the current trend is Canada's role. Early 2025/26 data suggest that Canadian shipments account for much of the recent increase in U.S. edible tallow imports. Structurally, this makes sense. Canada benefits from geographic proximity, integrated North American livestock and rendering industries, relatively efficient logistics for food-grade materials, and compatible regulatory systems. As industrial demand tightens the North American rendered fats balance, Canadian supply is increasingly important for meeting specific food-grade requirements in the U.S. market.

Despite growing attention to edible tallow, the broader market story remains firmly centered on industrial consumption. The U.S. biofuel sector continues to be the dominant force reshaping global tallow trade, influencing pricing structures, redirecting trade flows, and increasing global competition for limited rendered fat supplies. The United States has effectively transitioned from a historic exporter into the world’s largest structural buyer, fundamentally altering the balance of the international market.

Still, the sudden acceleration in edible tallow imports serves as another reminder that the effects of biofuel-driven demand are no longer confined solely to industrial markets. They are increasingly spilling over into food-use channels as well, creating new trade patterns and reshaping how the broader fats and oils complex functions in the United States.

More details on global tallow supply and demand, as well as 2026/27 outlook, can be found in the report here: Global Tallow and Greases Outlook 2026/27 (April 2026) | Demetrica Analytics

Comments