U.S. Soybean Exports 2025/26: A Season Without China...So Far (18 November 2025)

- agatakingsbury

- Apr 26

- 4 min read

The 2025/26 marketing year is turning into a live experiment: What does U.S. soybean trade look like without China?

So far, the answer is: surprisingly resilient, as long as the U.S. stays competitively priced.

Because up to mid-November, according to USDA AMS inspections, the United States has shipped almost 10 million metric tons of soybeans to markets other than China, and zero to China itself. That is not a normal pattern. The only recent parallel is 2018/19, during Trade War 1.0, when China largely stepped away from the U.S. market and the United States had to lean hard on the rest of the world.

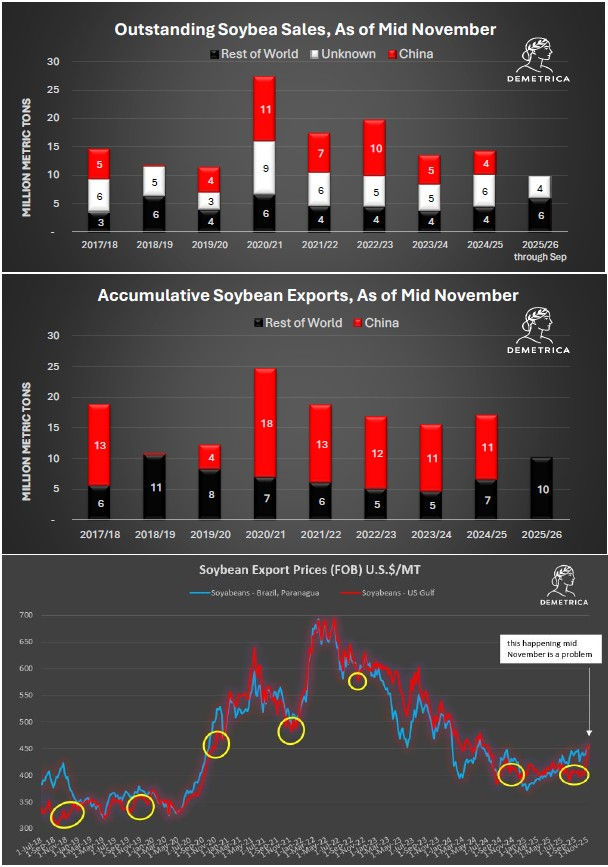

Outstanding Sales: Echoes of Trade War 1.0

The first chart, “Outstanding Soybean Sales, As of Mid November,” tells the story clearly.

In most years, outstanding sales to non-China destinations (Rest of World + Unknown) sit in the mid-single digits by mid-November.

In 2020/21 and 2022/23, when China was aggressively buying, the red “China” bar towers over everything else.

But in 2018/19 and now again in 2025/26, the composition flips:

China absent,

while Rest of World + Unknown together reach around 10 MMT of outstanding sales, as high or higher than in the China-heavy years.

And remember, that’s based on data only through September 25, because the government shutdown froze Export Sales reporting right when the season was ramping up. Even with incomplete data, the message is loud:

When China doesn’t show up, other buyers step in, as long as the U.S. is cheap enough.

Actual Shipments: A Great ROW Start

The second chart, “Accumulative Soybean Exports, As of Mid November,” confirms that these aren’t just paper sales.

By mid-November 2025/26:

The U.S. has shipped around 10 MMT of soybeans to the Rest of World,

None to China,

And that ROW volume is comparable only to 2018/19.

In most “normal” years:

China dominates early shipments: 11-18 MMT by mid-November.

Rest of World volumes hover in the 5-7 MMT range.

This year is the mirror image of 2018/19: ROW at record levels, China at zero.

The United States can move a significant amount of beans without China (not all obviously) but only if it stays competitive on price.

The Price Game: How We Keep Losing Our Edge

And that’s where the third chart comes in: “Soybean Export Prices (FOB) – Brazil vs. U.S.”

Historically, the seasonal pattern is pretty clear:

Around U.S. harvest (Oct-Nov), Gulf FOB prices usually trade at a discount to Brazil Paranaguá.

That discount often extends through November-December, sometimes into January, and has been the core U.S. seasonal shipping window.

Brazil is between crops and the United States uses that window to push volume.

The yellow circles on the chart highlight periods where the United States enjoyed a meaningful discount to Brazil.

In the last few weeks, that pattern has been breaking down.

If you have been tracking recent news, the market got hyped over seven cargoes of soybeans reportedly booked by China for Dec-Feb shipment. Seven cargoes. Not a structural comeback, more like snacks.

Yet every time someone whispers “China is back,” the market reacts:

Futures jump

Gulf FOB offers rise

And the United States quickly loses the price advantage it needs to keep non-China demand flowing.

So here we are, finishing harvest in 2025/26, the moment when the United States should be at its most competitive point, and yet U.S. soybeans are not particularly cheap versus Brazil.

That is not a good place to be.

The Debate: Crumbs vs. Customers

We ask a simple question:

Why is the market losing its mind over crumbs, while ignoring the customers who are actually buying and shipping volume?While everyone was cheering first three cargos and then seven cargoes, the Rest of World was doing the heavy lifting, quietly booking and loading beans, pushing ROW shipments to record levels, and sustaining U.S. export flows without China.

Every time prices spike on “China headlines”:

Non-China buyers step back because the U.S. is no longer competitive.

Domestic crushers pay more than they otherwise would, squeezing margins.

And the U.S. squanders its best seasonal window for winning and retaining long-term customers.

It’s a kind of “hostage dynamic”:

China does just enough business - or makes just enough noise - to move prices, while most of the actual buying gets done in Brazil.

What the 2025/26 Data Is Really Telling Us

Putting all three charts together, a few key points emerge:

Demand is there.

When the United States is priced right, non-China importers are more than willing to take U.S. beans. Marketing year 2025/26 ROW shipments and outstanding sales are proof.

China is not irreplaceable in the early season.

That doesn’t mean China isn’t important, it absolutely is for full-year totals, but early-season flow can be maintained without them, if price works.

Narratives are moving prices more than fundamentals.

A handful of cargoes and vague talk of “deals” are enough to change the tone of the market, even when official Chinese statements and USDA corrections (like the recent reduction of a daily sales announcement) tell a much more cautious story.

The U.S. keeps undercutting its own competitiveness.

By allowing every China rumor to re-price the market higher, we’re effectively pricing out the very customers who are showing up, while giving China even more optionality to sit back and wait.

Where Do We Go From Here?

None of this is a call to ignore China. It’s simply a reminder that:

Data beats narrative.

Price beats wishful thinking.

The 2025/26 marketing year so far shows that the U.S. export engine can run without China and even run better to other markets as long as we maintain a harvest-season discount to Brazil.

The risk is that we keep reacting to every China headline, blow out that discount, and then wonder why export inspections slump later in the season.

Going forward, the key questions for the balance sheets are:

Will China step in meaningfully later in the year, or keep “managing expectations” while leaning on Brazil?

Can the United States hold onto these new and expanded non-China relationships if price volatility keeps chasing them away?

And will USDA’s export projections eventually acknowledge that the shape of demand is changing, not disappearing?

For now, the charts tell a clear story:

When the United States keeps its price edge, the rest of the world buys.When we trade that edge for a headline, they don’t.

And that may be the most important lesson of this “year without China” so far.

Comments