U.S. Tallow Imports: From Afterthought to Global Demand Driver (22 April 2026)

- agatakingsbury

- Apr 26

- 3 min read

A Decade of Structural Change

For most of the past decade, U.S. tallow imports were relatively small and largely irrelevant in the global context. Volumes remained modest through the mid-2010s, reflecting a market where domestic production was sufficient to meet demand and exports were still a meaningful outlet.

That dynamic has completely changed.

Starting around 2019–2020, imports began to trend higher, but the real inflection point came after 2021. Since then, volumes have surged, reaching over 1 million metric tons in 2024/25. The scale and speed of this growth point to more than just cyclical demand — they signal a fundamental shift in how the market functions.

Biofuels as the Core Driver

The key force behind this change is the rapid expansion of biofuel production in the United States.

Renewable diesel and, increasingly, sustainable aviation fuel (SAF) have created strong demand for low-carbon feedstocks. Inedible tallow fits this role particularly well, making it one of the preferred inputs for these fuel pathways.

As capacity expanded, domestic supply alone was no longer sufficient. Imports became necessary — and then critical.

What was once a secondary flow turned into a primary supply channel.

The Shift in Market Role

The implication is clear: the United States has transitioned from a net exporter to a major net importer of tallow.

This shift has had a ripple effect across the global market:

Exporters now target the United States as a key destination

Trade flows have reoriented toward North America

Global availability has tightened as more supply is absorbed domestically

In effect, U.S. demand is no longer just a part of the market — it is shaping the market.

Recent Developments: Tariffs and Trade Flow Adjustments

The most recent data adds another layer to the story.

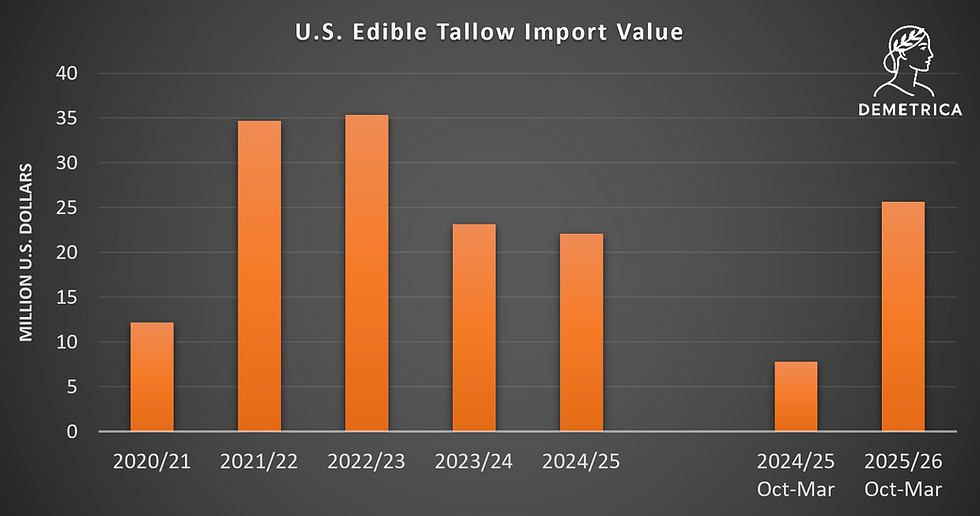

In mid-2025, the United States introduced tariffs on Brazilian tallow, which had become a major source of imports. At first glance, this might suggest a potential slowdown in total import volumes.

However, early data for the 2025/26 marketing year (October–February) tells a different story.

Total imports are only slightly lower year-on-year, indicating that overall demand remains strong. Instead of declining, the market has adjusted.

Imports from Brazil have fallen sharply

Volumes from other suppliers have increased

The overall balance has remained relatively stable

This highlights an important point: the U.S. biofuel sector is not easily constrained by supply from a single origin. If one source becomes less competitive, material is sourced elsewhere.

What This Means for the Market

The chart illustrates more than just growth — it shows a structural transformation.

Several key conclusions emerge:

U.S. demand has become the primary driver of global trade flows

Imports are now essential to balancing the domestic market

Supply chains are flexible and capable of adapting to policy changes

The market is increasingly influenced by biofuel economics rather than traditional uses

Perhaps most importantly, this does not appear to be a temporary development. The scale of investment in renewable fuels suggests that demand for tallow will remain elevated, keeping the United States at the center of the global market.

Final Thought

What was once a relatively niche commodity flow is now a key component of the global energy transition.

And as this chart shows, that shift is already well underway.

(This analysis is part of the Global Tallow & Greases Market Outlook 2026/27 report available for purchase)

Comments