US-India Trade Deal Talk: Why Bulk Crops Are Unlikely? (4 February 2026)

- agatakingsbury

- Apr 26

- 4 min read

U.S. Vegetable Oil Trade

U.S. Vegetable Oil Import and Export

US-India Trade Deal Talk: Why Bulk Crops Are Unlikely and Why Soybean Oil Is the Real (But Limited) Story

Talk of a potential U.S.-India trade deal has re-energized agricultural markets. Early price reactions, particularly in soybean oil, suggest optimism that U.S. farm exports to India could expand meaningfully. Headlines, however, tend to flatten a far more complex reality. To understand what’s plausible (and what isn’t), it helps to separate politics, social constraints, and market structure from short-term price signals.

This discussion does exactly that: first by explaining why bulk crop exports - especially GMO food crops - are highly unlikely, then by examining soybean oil as the most realistic agricultural outlet, and finally by grounding expectations in actual U.S.-India trade flows, supply limits, policy uncertainty, and pricing dynamics.

Why Bulk Agricultural Crops Face a Hard Stop in India

India is home to one of the largest populations of smallholder farmers in the world. Agricultural policy there is inseparable from food security, employment, and political stability. Any trade discussion that assumes India will open its doors to large volumes of U.S. bulk crops ignores this fundamental reality.

GMO constraints are not just regulatory - they’re political

Food-use GMOs remain tightly restricted in India. While non-food applications may occasionally be discussed, opening the market to bulk GMO food crops would be deeply controversial. The issue isn’t only biosafety, it’s livelihoods.

India’s history shows that farm income shocks have real social consequences, including protests and long-term political fallout. Policies perceived as undermining domestic farmers can escalate quickly. From that standpoint alone, allowing bulk GMO commodities to flood the domestic market would be politically explosive, arguably impossible.

Bottom line: any serious U.S.-India agricultural expansion is unlikely to be crop-based. The pathway, if it exists, must lie elsewhere.

Why the Conversation Shifts to Vegetable Oils

If crops are politically constrained, vegetable oils present a very different case.

India’s structural deficit is in oils, not oilseeds

India is largely self-sufficient in oilseeds such as soybean, rapeseed (canola), or peanut (groundnut). It also produces enough protein meal domestically and does not need large imports in that category. What India lacks is vegetable oil.

Palm oil and soy oil dominate India’s import basket, with sunflower oil becoming increasingly important in household diets. This structural deficit is long-standing and widely acknowledged.

Crucially, India already imports soybean oil, notably from Argentina. From a regulatory and dietary standpoint, sourcing soy oil from the U.S. would not be a leap.

And it has already happened.

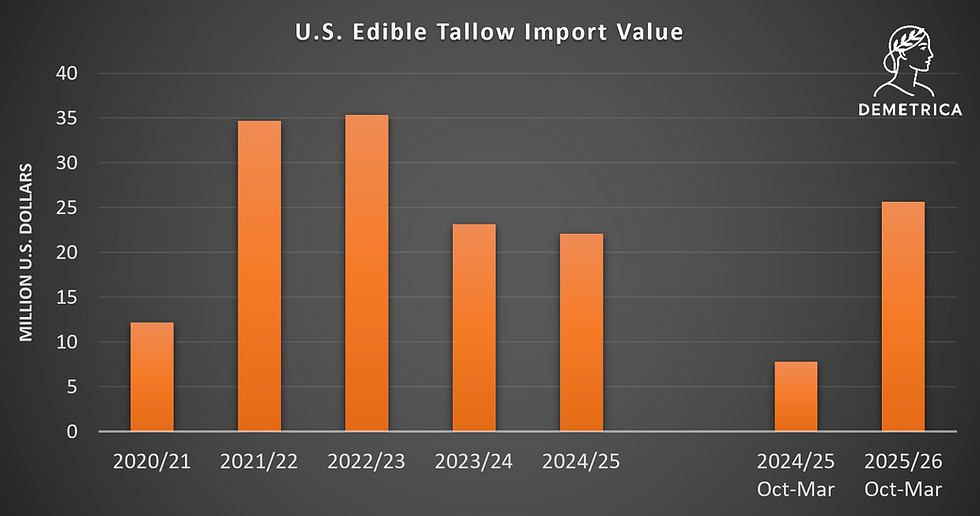

A Key Data Point: U.S. Soybean Oil Exports to India Are Real

In marketing year 2024/25, the United States exported approximately 238,000 metric tons of soybean oil to India. That’s a meaningful volume, not massive, but large enough to demonstrate that the trade lane can function under the right conditions.

This data point matters because it shows that soy oil can fit into the U.S.-India trade relationship in a way that bulk crops cannot.

But context matters even more.

The Long Arc of U.S. Soybean Oil Exports

Historically, U.S. soybean oil exports exceeded 1 million metric tons. After a period of plateau, they collapsed to historical lows over the past decade. The reason wasn’t lost competitiveness abroad; it was explosive growth in domestic demand.

Biofuels changed everything

Food use has always absorbed a portion of U.S. soy oil production. What changed the balance was biofuels. Today, the majority of U.S. soy oil is consumed domestically by food and fuel markets. This structural shift is visible in the chart:

Exports trend downward as biofuel demand rises

Imports of alternative oils increase to fill domestic gaps

Export availability becomes episodic rather than structural

Why Exports Rebounded in 2024/25

The export uptick last year, including shipments to India, was not driven by surplus production. It was driven by timing. Two factors temporarily softened domestic competition for soy oil:

Biofuel policy uncertainty

Prolonged uncertainty around renewable fuel incentives slowed some domestic demand and delayed investment decisions.

Growth in used cooking oil (UCO) imports

Cheaper imported UCO captured a larger share of biofuel feedstock demand, displacing some soy oil usage in the short term.

That combination created a window for exports.

Why That Window Is Narrowing

The same charts that explain last year’s rebound also show why it may not last.

UCO growth is slowing

While UCO imports continue to rise, growth has moderated amid:

Fraud allegations and traceability concerns

Sustainability scrutiny

Changes to tax credit eligibility for imported feedstocks

Domestic demand remains strong

At the same time, domestic demand for soy oil as food and fuel remains robust. According to USDA projections, soybean oil exports are expected to decline in 2025/26, reflecting tighter domestic balances and less displacement from UCO.

Policy uncertainty freezes expansion

Crush capacity expansion, critical to increasing oil supply, has slowed as the industry waits for clearer signals on biofuel policy. Promised guidance has been repeatedly delayed, now into March 2026. Without policy clarity, capital stays on the sidelines.

Price: The Final Constraint

Even if India wants more U.S. soy oil, and even if a trade deal lowers friction, price still rules.

Domestic demand competes directly with exports, lifting U.S. soy oil prices. India remains a highly price-sensitive buyer with access to multiple origins. Deal or no deal, no importer wants to pay more than necessary when alternatives exist.

What the United States Actually Exports to India Today

This brings expectations back to reality. Historically, U.S. agricultural exports to India have focused on:

Ethanol

Tree nuts (primarily almonds)

Apples

Dried lentils

Small volumes of dairy products

These are higher-value, targeted products that do not threaten India’s small farmers or domestic food security. Soy oil, if included, fits this pattern far better than bulk GMO crops, but it remains constrained by supply, policy, and price.

Bottom Line

Bulk GMO crop exports to India are politically and socially unrealistic. Vegetable oils, particularly soybean oil, are the most plausible agricultural addition to a U.S.-India trade framework.

But last year’s soybean oil shipments were enabled by temporary conditions, not structural surplus. With domestic demand strong, policy uncertainty unresolved, and prices under upward pressure, expectations for a large, durable expansion in U.S. soy oil exports to India may be running ahead of reality.

The trade lane exists. The question isn’t access, it’s how much supply the United States can sustainably spare, at what price, and for how long.

That’s the conversation worth having.

Data sources: USDA PSD, U.S. Census, Demetrica projections

Comments